Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

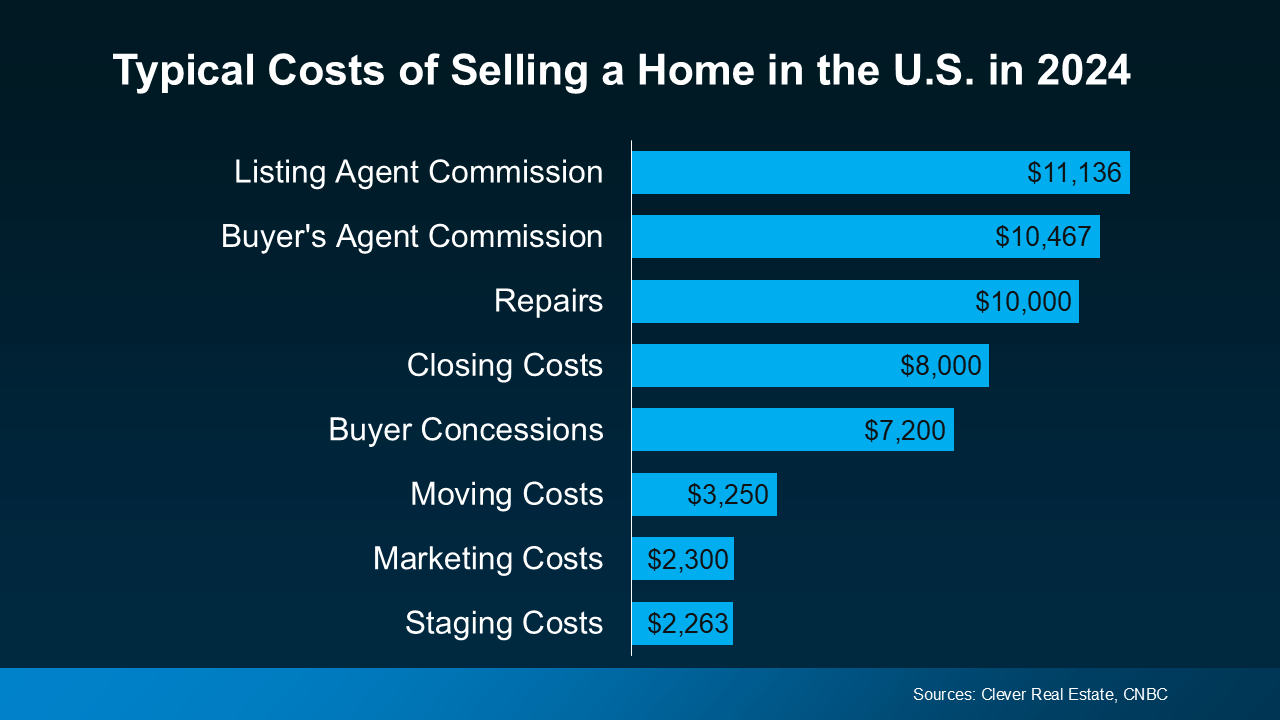

How Much Does It Cost To Sell My House?

If you’re toying with the idea of selling your house, you’re probably wondering how much it’ll cost. To be honest, the final number will depend on several factors like the offer you accept, if you help with your buyer’s closing costs, how many repairs you tackle, and more.

So, to give you a ballpark of what to expect, here’s some information on a few of the expenses you’ll want to be ready for (see graph below):

But here’s something that puts those costs into perspective. Most homeowners today have a substantial amount of equity built up in their homes, and that means they stand to make significant gains when they sell. Chances are, you do too. This can help quickly recoup these selling costs. You may even have enough equity leftover to put some toward your next home purchase too.

Let’s dive into a few of the costs from the graph above, so you have a bit more context on what they include and where you may be able to save some money, when it makes sense.

Closing Costs and Commission

These are the fees you’ll pay at the closing table to cover various aspects of the sale. You’ll have your own closing costs and you may even offer to pay some of the buyer’s as a concession. As U.S. News Real Estate explains:

“Closing costs are fees that are paid to finalize the transaction and transfer ownership of the home to the buyer . . . Sellers can expect to pay 2% to 4% of the sale price of the home in fees and taxes on top of the agent commission. Based on the national median home sale price, this means that closing costs in 2023 for sellers are about $7,740 to $15,480. . .”

Taxes are going to vary by state and agent commissions depend on what you agree upon upfront. And keep in mind, that the numbers in the chart above are just an example, not exact figures. Not to mention, if you put money toward things like your property taxes, mortgage escrow, etc. as part of your current mortgage payments – there’s a chance you’ll get a credit back at closing that can help offset some of these selling expenses.

Pre-Listing Inspection and Repairs

One optional step some sellers take is having a pre-listing inspection. It gives you an idea of what may pop up later on in the buyer’s inspection – because those are the items a buyer may ask you to toss in a credit (or concession) to cover later on.

This allows you to get a jump on any repairs and tackle them before you list, so your house is set up to impress from the start.

Again, if you want to skip this step, an agent can help. They’ll be able to give you advice on things like paint colors, small cosmetic repairs, what buyers are looking for, and whether it’s worth tackling anything else ahead of time. This will help make sure you’re spending money on things that are most likely to net you a solid return on your investment.

Home Staging

As inventory grows, you may want to take a few extra steps to make sure your house stands out. Staging is an optional way to make sure your house shows well. It can include bringing in rental furniture if the house is vacant or art to warm up the walls. Some staging can even be done virtually once the photos are taken. But, in general, how much does it cost? According to Bankrate:

“Home sellers typically pay somewhere between $782 and $2,817 in home staging costs . . . but the price tag can vary widely.”

If you want to skip this step, you could opt to lean on your agent’s advice for what looks good and what may feel cluttered. A great agent will suggest things like removing a chair to open up the flow of a room, laying down a rug to add warmth to a space, or taking down photographs to de-personalize strategic areas.

Why Leaning on an Agent Is Key

If you’re looking to cut down on your costs, you have options. But be careful of where you trim. You may be able to skip staging or a pre-listing inspection since those are optional, but you don’t want to skimp and sell without a pro.

An agent is your go-to expert throughout the transaction. They’ll offer customized advice every step of the way, including how to stage the house and what repairs to tackle. This can help you avoid hiring an outside stager or having to pay for a pre-listing inspection.

But that’s not the only way your agent adds value. They’ll also create tailored marketing and pricing strategies that’ll highlight the house’s best assets and any work you did to get the home show ready. And that can actually help your house sell for more in the long run.

Bottom Line

Want a better picture of what you should expect when you sell your house? Let’s have a conversation and walk through it together.

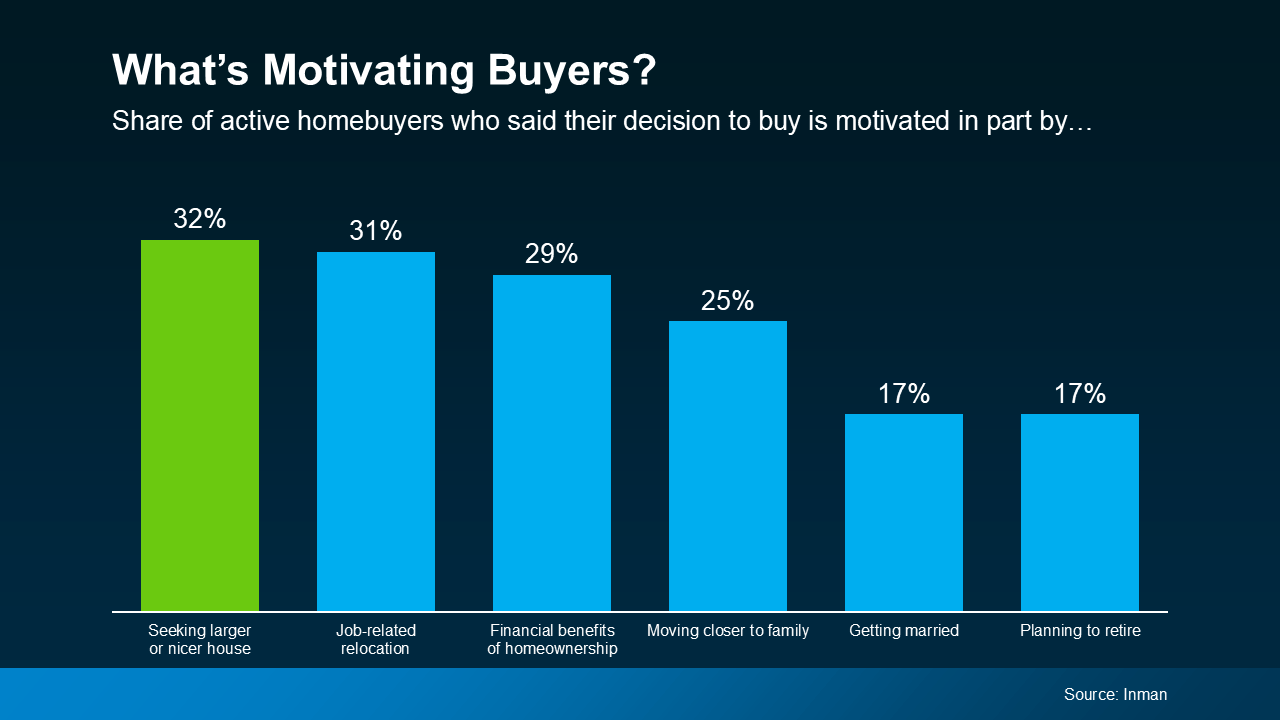

Now’s the Time To Upgrade to Your Dream Home

If you’ve been wanting to sell your house and move up to a bigger or nicer home, you’re not alone. A recent Inman survey reveals the top motivator for today’s homebuyers is the desire for more space or an upgraded home (see graph below):

But there’s also a good chance you, like many other people, have been holding off on that goal because of recent market challenges. It makes sense – when you’re planning an upgrade that could increase your monthly housing costs, affordability has a huge impact on when you make your move. But there’s good news: now’s actually a great time to make that move happen. Here’s why.

You Have a Lot of Equity To Leverage

One of the key benefits in today’s market is the amount of equity you’ve likely built up in your current house over the years. Even with recent shifts in the housing market, national home prices have steadily grown, adding to the equity homeowners have today. Selma Hepp, Chief Economist at CoreLogic, explains it well:

“Persistent home price growth has continued to fuel home equity gains for existing homeowners who now average about $315,000 in equity and almost $129,000 more than at the onset of the pandemic.”

What does that mean for you? If you’ve been in your home for a few years, you’re probably sitting on a significant amount of equity. You can put that toward the down payment on your next home, helping keep the amount you borrow within a comfortable range.

This can make upgrading more achievable than you might think. If you’re curious how much you’ve built up over the years, ask your real estate agent for a professional equity assessment.

Mortgage Rates Have Fallen, Boosting Your Purchasing Power

And there’s another big reason why now’s a great time to make your move: mortgage rates are trending down. Lower rates can help make your future monthly payments more manageable, and they also increase your purchasing power. As Nadia Evangelou, Senior Economist and Director of Real Estate Research at the National Association of Realtors (NAR), points out:

“When mortgage rates fall, the interest portion of monthly payments decreases, which lowers the total payment. This makes it easier for more borrowers to . . . qualify for mortgages that may have been unaffordable at higher rates.”

That gives you more flexibility when shopping for homes and may allow you to afford a house at a price point that was previously out of reach. A trusted lender can work with you to figure out the best plan for your budget.

Bottom Line

If you’re ready to sell your current home and find the bigger, nicer home you’ve been dreaming of, don’t wait. Your equity, paired with lower mortgage rates, puts you in a great position to make that move today.

To make the best decisions and get the most out of your current market advantage, let’s connect so you have an expert guide through every step of the homebuying process.

Why Buying Now May Be Worth It in the Long Run

Should you buy a home now or should you wait? That’s a question a lot of people have these days. And while what’s right for you is going to depend on a lot of different factors, here’s something you’ll want to consider as you make your decision.

As soon as you buy, you’ll start gaining equity. And you’d be surprised how quickly that can add up – even with more moderate home price appreciation.

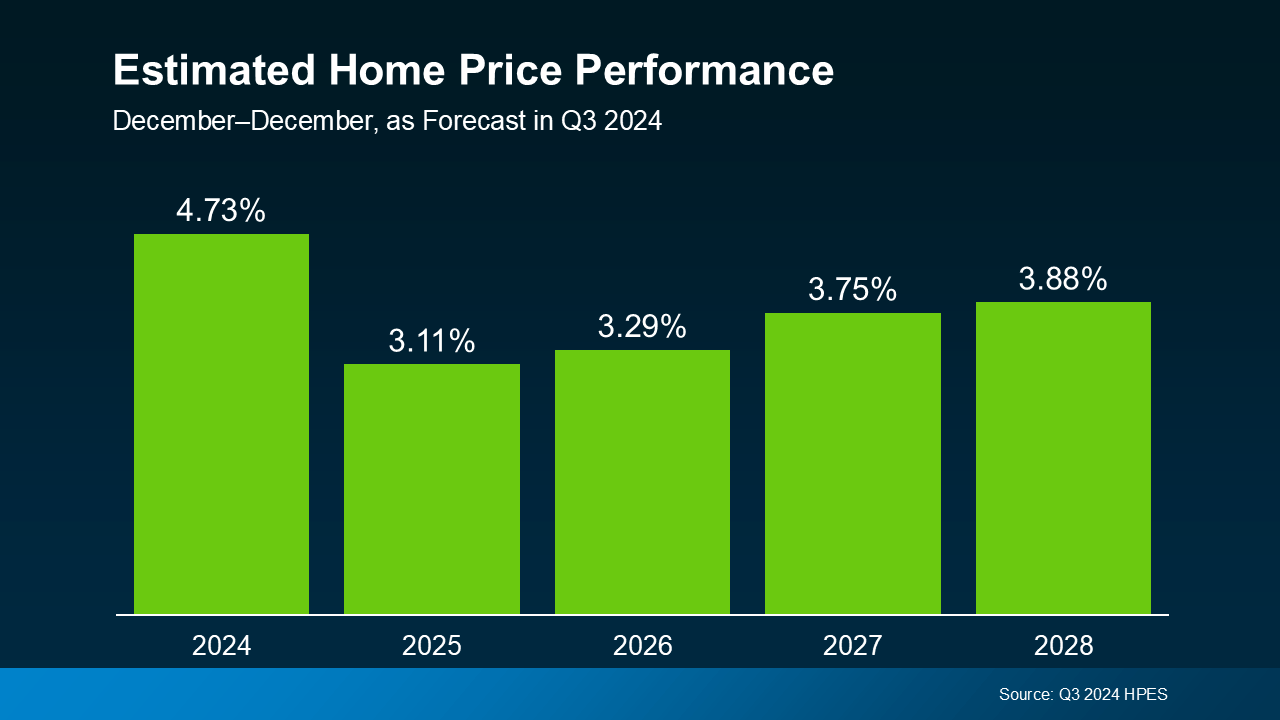

Each quarter, Fannie Mae releases the Home Price Expectations Survey. It asks over one hundred economists, real estate experts, and investment and market strategists what they forecast for home prices over the next five years. In the latest release, experts project prices will continue to rise nationally through at least 2028 (see the graph below):

While home prices are going to vary from one local area to the next, this shows they’re expected to keep going up nationally. The size of the increase varies from year-to-year, but the important takeaway is that prices are forecast to rise every single year – just at a moderate pace.

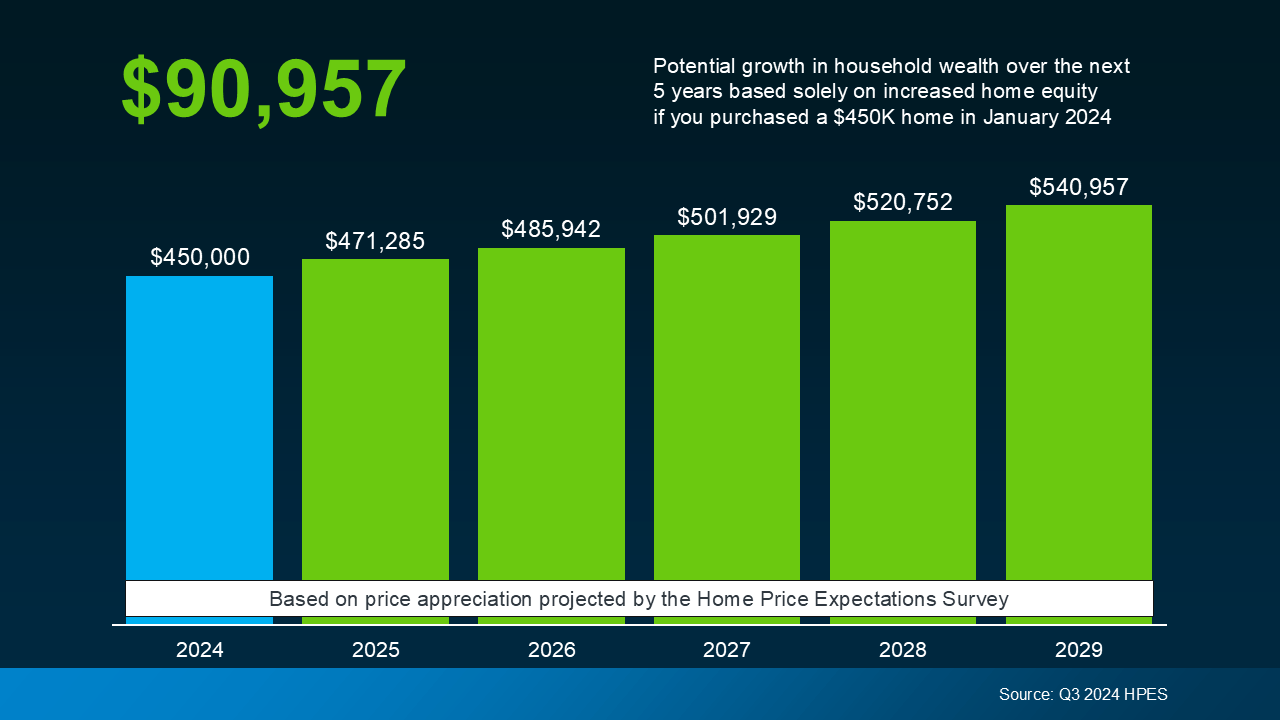

And while rising home prices may not sound great right now, once you own a home, that growth will be a big bonus for you. Here’s a look at what you stand to gain equity-wise once you buy. The graph below uses a typical home’s value and those HPES projections to show how much equity is at stake:

If you bought a $450,000 home at the beginning of this year, based on that starting value and the expert forecasts from the HPES, you could gain more than $90,000 in household wealth over the next five years. That’s significant.

So, if you’re ready and able to buy, and growing your wealth is important to you, you’ve got an opportunity in front of you. And now that mortgage rates have fallen, it may be time to consider making a move.

To talk more about your options and what makes sense, lean on a pro. They’ll be able to tell you what home prices are doing in your area and what that means for your move (and your future equity). The Mortgage Reports says:

“Given the intricacies of the current market, it’s more important than ever to stay informed and up to date about housing market conditions. Whether you’re looking to buy or sell in the remaining months of 2024, having a professional guide you through the process can make all the difference.”

Bottom Line

The decision to buy now or wait is a very personal one, but it’s valuable to have an expert’s perspective. They won’t push you, but they will explain things you may not have considered, like the equity that’s at stake.

If you want help weighing your options and thinking through how the current market factors in, let’s connect.

Is Your House Priced Too High?

Every seller wants to get their house sold quickly, for as much money as they can, with as few headaches as possible. And chances are, you’re no different.

But did you know one of the biggest things that could jeopardize your success is the asking price for your home? Pricing your house correctly is one of the most crucial steps in the selling process.

So, how do you know if you’re missing the mark? Here are four signs your high asking price might be turning potential buyers away—and why leaning on your real estate agent is the best way to course correct.

1. You’re Not Getting Many Showings or Offers

One of the most obvious signs your house may be overpriced is a lack of showings. If it’s been on the market for several weeks and only a few buyers have come to see it—or worse, you haven’t gotten any offers—it could be a clear indication the price isn’t matching up with what buyers expect. Because buyers who have been looking for a while can easily spot (and write off) a home that seems overpriced.

Your real estate agent will coach you through this, so lean on their experience for what you may want to try to bring more buyers in, including considering a price cut.

2. Buyers Have Consistent Negative Feedback after Showings

And if after the showings you do have, comments from the potential buyers aren’t great, you may need to course correct. Feedback from showings is an important part of understanding how buyers see your house. If they consistently say it’s overpriced compared to other homes they’ve seen, it’s time to reconsider your pricing strategy.

Your agent will gather and analyze this feedback for you, so you can look at how your house stacks up in the market. They can also suggest specific improvements or staging changes to better justify your asking price, or recommend one that aligns with today’s buyer expectations. As the National Association of Realtors (NAR) explains:

“Based on all the data gathered, agents may make adjustments to the initial price recommendation. This could involve adjusting for market conditions, property uniqueness, or other factors that may impact the property’s value.”

3. It’s Been on the Market for Too Long

And that lack of interest is ultimately going to lead to it sitting on the market without any serious bites. The longer it lingers, the more likely it is to raise red flags for buyers, who may wonder if something is wrong with it. Especially in today’s market with growing inventory, a long listing period means your house is stale – and that makes it even harder to sell.

Your real estate agent will be able to give you perspective on how quickly other homes in your area are selling and walk you through what’s working for other sellers. That way you can decide together if there’s something you want to do differently. As a Bankrate article says:

“Check with your agent about the average number of days homes spend on the market in your area. If your listing has been up significantly longer than average, that may be a sign to reduce the price.”

4. Your Neighbor’s House Sold Without an Issue

And here’s the last one to watch out for. If similar homes in your area are selling faster than yours, it’s a clear sign that something is off. This could be due to things like a lack of upgrades, outdated features, or a less desirable location. Or, it may be priced too high.

Your agent will keep you up to date on your competition and what changes, if any, you need to make your home more competitive. They’ll offer advice on small updates that could increase your home’s appeal or how to adjust your strategy to reflect the reality of the market today.

Bottom Line

Pricing a home correctly is both an art and a science. It requires a deep understanding of the market and buyer psychology. And when the price isn’t drawing in buyers, there’s no better resource than your agent on what you may want to do next.

The Best Time To Buy a Home This Year

A shift is underway in the housing market this season. And if you’ve been sitting on the sidelines waiting for the right moment to jump back into your homebuying search, this is a great time to do it. That’s because the best week to buy a home this year is just around the corner. Your sweet spot is here.

The experts at Realtor.com study seasonal trends to figure out the ideal week for homebuyers:

“Nationally, the best time to buy in 2024 is the week of Sept. 29–Oct. 5. This week historically has shown the best balance of market conditions that favor buyers. Inventory tends to be high, prices are below peak levels, demand is waning, and the pace of the market slows to a more manageable speed.”

In addition to the historical trends and typical seasonality that Realtor.com looks at, there are also clear indicators in today’s market data that you’ll see better conditions right now than you would have over the last few years.

Mortgage rates just hit their lowest point in 19 months, and that goes a long way to help with your purchasing power and affordability. Andy Walden with Intercontinental Exchange Inc. (ICE) points out:

“Recent easing in mortgage rates brought some much-sought relief to prospective homebuyers. Along with a general cooling in home price growth, rates falling below 6.5 percent made August the most affordable month for housing since February.”

And Ralph McLaughlin, Senior Economist at Realtor.com, explains that it’s not just rates that have improved – inventory has too:

“The number of homes actively for sale continues to be elevated compared with last year, growing by 35.8%, a 10th straight month of growth, and now sits at the highest since May 2020.”

That should give you more options. At the same time, sellers now have to compete with each other for your attention. That means they’ll be more likely to negotiate because they know their house will sit on the market longer if they don’t. As Zillow says:

“Buyers waiting on the sidelines could find that early fall presents a ‘sweet spot,’ where there’s less competition from other buyers, more motivated sellers and lower interest rates to finance their purchases.”

Bottom Line

If you want to make sure you’re ready to take advantage of this sweet spot, let’s connect and start the prep work now. Maybe it’s time to get off the sidelines and into the action.

The Surprising Amount of Home Equity You’ve Gained over the Years

There are a number of reasons you may be thinking about selling your house. And as you weigh your options, you may find you’re unsure how you’re going to deal with one thing about today’s housing market – and that’s affordability. If that’s your biggest concern, understanding how much equity you have in your house could help make your decision that much easier. Here are two key factors that have a big impact on your equity.

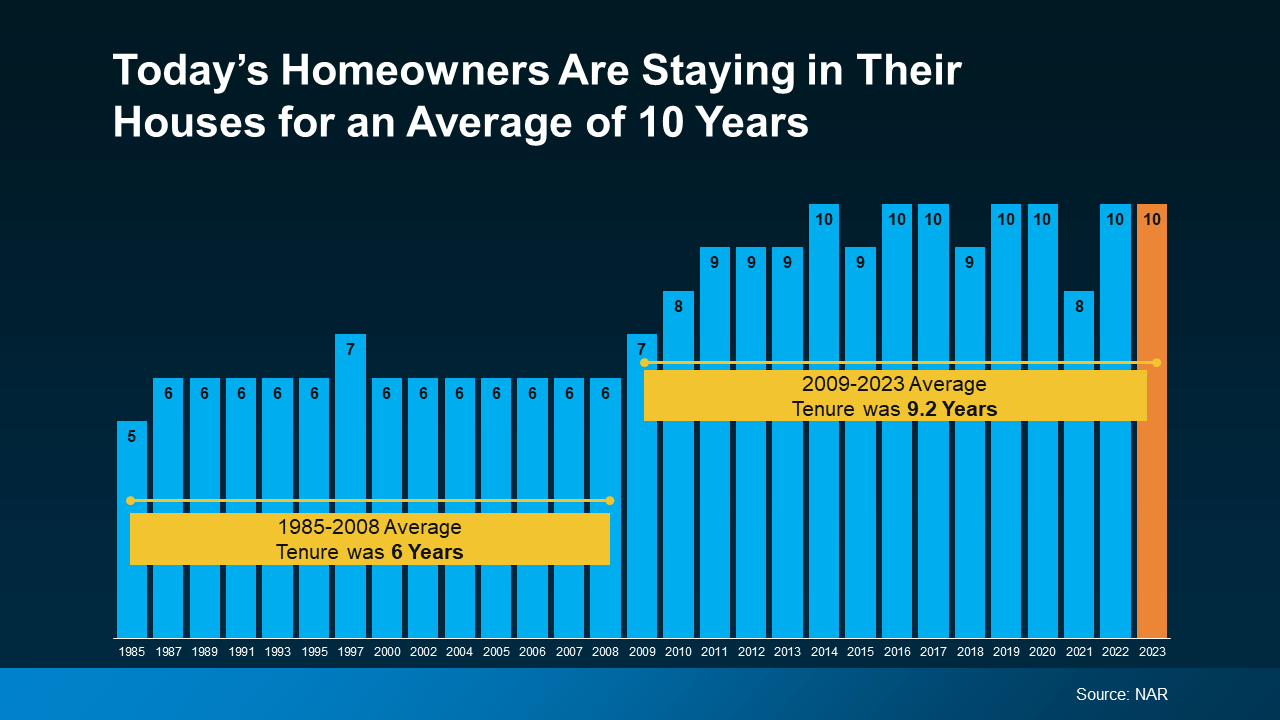

How Long You’ve Been in Your Home

First up is homeowner tenure. That’s how long homeowners live in a house, on average, before selling or choosing to move. From 1985 to 2009, the average length of time homeowners stayed put was roughly six years.

But according to the National Association of Realtors (NAR), that number has been climbing. Now, the average tenure is 10 years (see graph below):

Here’s why that’s such a big deal. You gain equity as you pay down your home loan and as home prices climb. And when you combine all of your mortgage payments with how much prices have gone up over the span of 10 years, that adds up. So, if you’ve lived in your house for a while now, you may be sitting on a pile of equity.

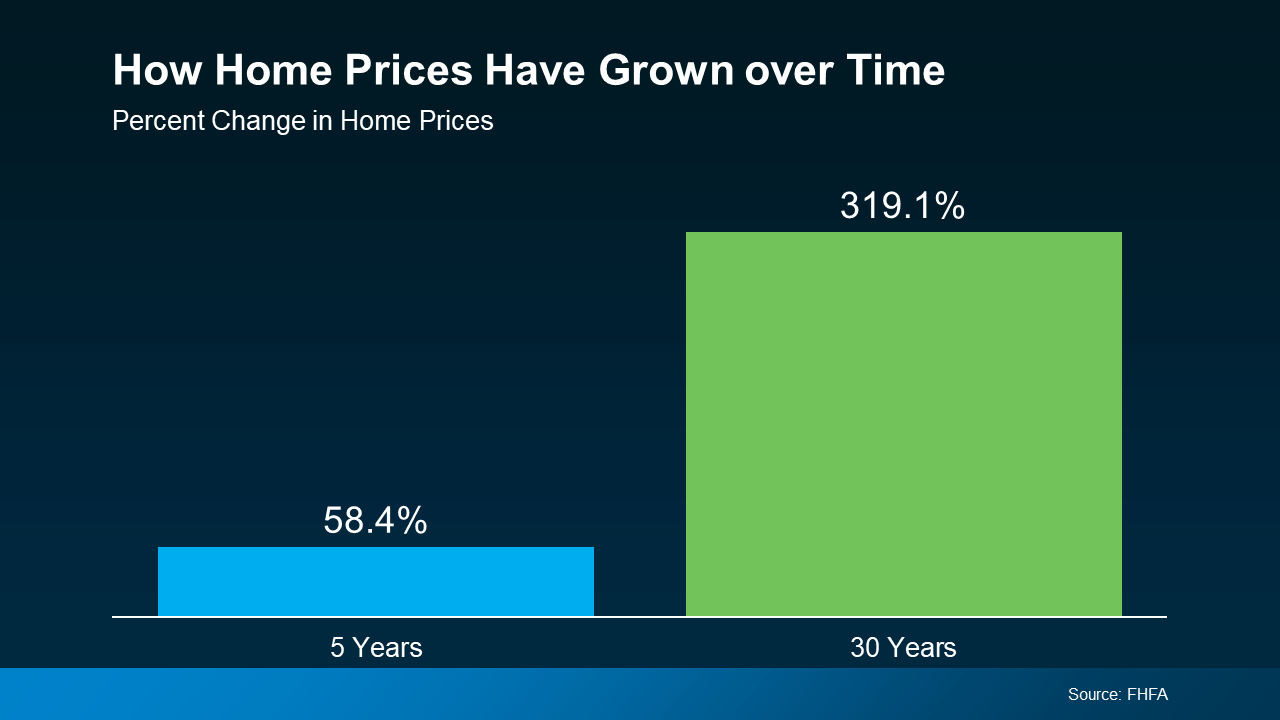

How Home Prices Appreciate over Time

To help show how much the price appreciation piece adds up, take a look at this data from the Federal Housing Finance Agency (FHFA) (see graph below):

Here’s what this means for you. While home prices vary by area, the typical homeowner who’s been in their house for five years saw it increase in value by nearly 60%. And the average homeowner who’s owned their home for 30 years saw it more than triple in value in that time.

Here’s what this means for you. While home prices vary by area, the typical homeowner who’s been in their house for five years saw it increase in value by nearly 60%. And the average homeowner who’s owned their home for 30 years saw it more than triple in value in that time.

Whether you’re looking to downsize, relocate to a dream destination, or move so you can live closer to friends or loved ones, your equity can be a game changer.

Bottom Line

If you want to find out how much equity you’ve built up over the years and how you can use it to buy your next home, let’s connect.

Should You Sell Now? The Lifestyle Factors That Could Tip the Scale

Are you on the fence about whether to sell your house now or hold off? It’s a common dilemma, but here’s a key point to consider: your lifestyle might be the biggest factor in your decision. While financial aspects are important, sometimes the personal motivations for moving are reason enough to make the leap sooner rather than later.

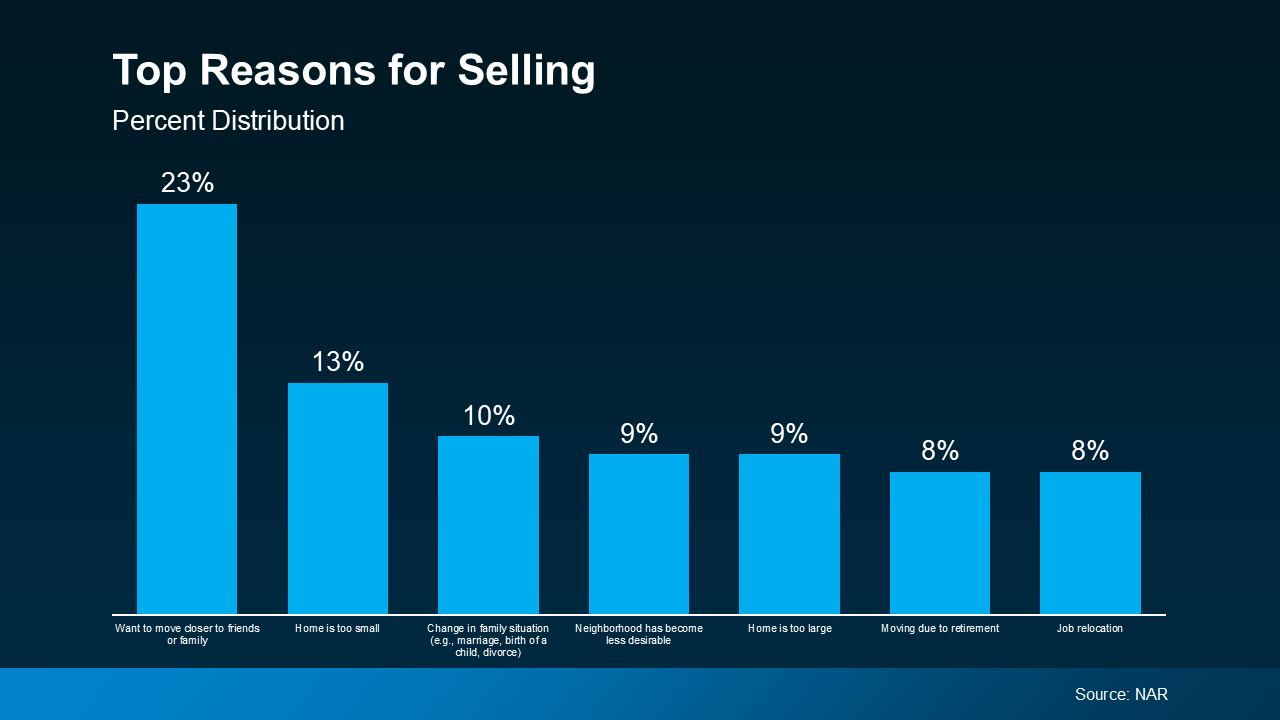

An annual report from the National Association of Realtors (NAR) offers insight into why homeowners like you chose to sell. All of the top reasons are related to life changes. As the graph below highlights:

As the visual shows, the biggest motivators were the desire to be closer to friends or family, outgrowing their current house, or experiencing a significant life change like getting married or having a baby. The need to downsize or relocate for work also made the list.

If you, like the homeowners in this report, find yourself needing features, space, or amenities your current home just can’t provide, it may be time to consider talking to a real estate agent about selling your house. Your needs matter. That agent will walk you through your options and what you can expect from today’s market, so you can make a confident decision based on what matters most to you and your loved ones.

Your agent will also be able to help you understand how much equity you have and how it can make moving to meet your changing needs that much easier. As Danielle Hale, Chief Economist at Realtor.com, explains:

“A consideration today’s homeowners should review is what their home equity picture looks like. With the typical home listing price up 40% from just five years ago, many home sellers are sitting on a healthy equity cushion. This means they are likely to walk away from a home sale with proceeds that they can use to offset the amount of borrowing needed for their next home purchase.”

Bottom Line

Your lifestyle needs may be enough to motivate you to make a change. If you want help weighing the pros and cons of selling your house, let’s have a conversation.

What Mortgage Rate Are You Waiting For?

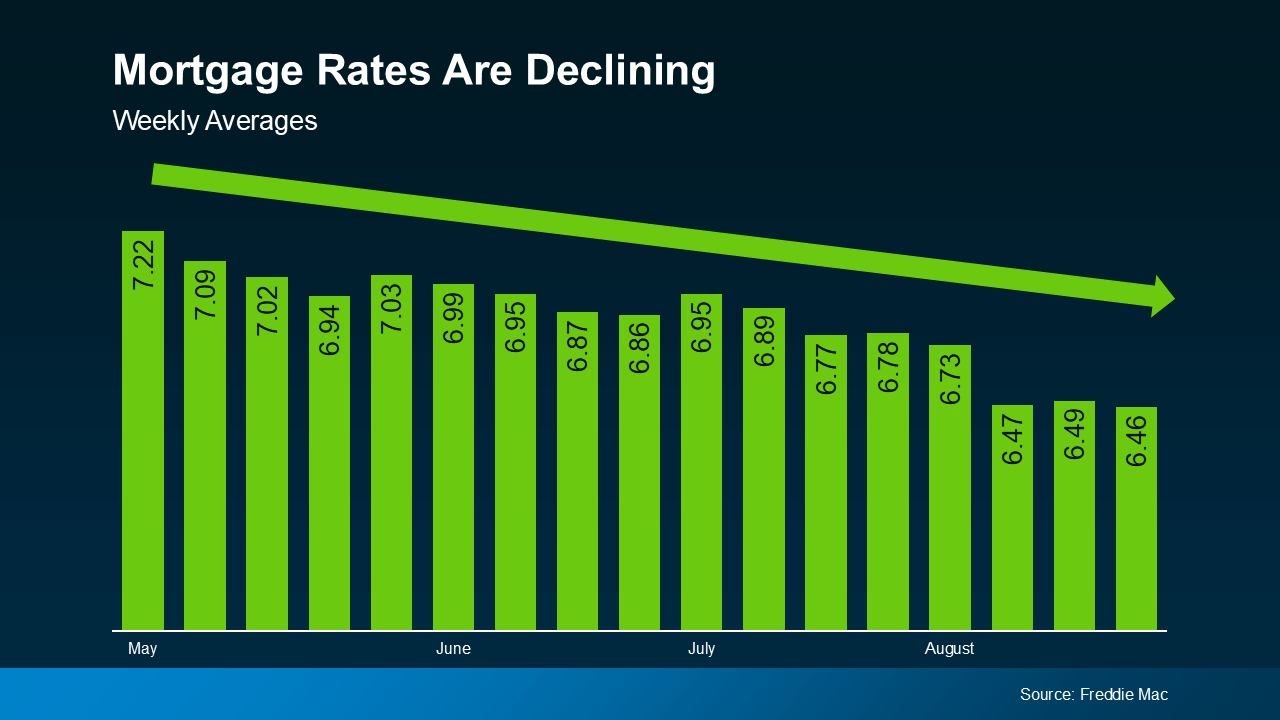

You won’t find anyone who’s going to argue that mortgage rates have had a big impact on housing affordability over the past couple of years. But there is hope on the horizon. Rates have actually started to come down. And, recently they hit the lowest point we’ve seen in 2024, according to Freddie Mac (see graph below):

And if you’re thinking about buying a home, that may leave you wondering: how much lower are they going to go? Here’s some information that can help you know what to expect.

Expert Projections for Mortgage Rates

Experts say the overall downward trend should continue as long as inflation and the economy keeps cooling. But as new reports come out on those key indicators, there’s going to be some volatility here and there.

What you need to remember is it’s not wise to let those blips distract you from the larger trend. Rates are still down roughly a full percentage point from the recent peak compared to May.

And the general consensus is that rates in the low 6s are possible in the months ahead, it just depends on what happens with the economy and what the Federal Reserve decides to do moving forward.

Most experts are already starting to revise their 2024 mortgage rate forecasts to be more optimistic that lower rates are ahead. For example, Realtor.com says:

“Mortgage rates have been revised slightly lower as signals from the economy suggest that it will be appropriate for the Fed to begin to cut its Federal Funds rate in 2024. Our yearly mortgage rate average forecast is down to 6.7%, and we revised our year-end forecast to 6.3% from 6.5%.”

Know Your Number for Mortgage Rates

So, what does this mean for you and your plans to move? If you’ve been holding out and waiting for rates to come down, know that it’s already happening. You just have to decide, based on the expert projections and your own budget, when you’ll be willing to jump back in. As Sam Khater, Chief Economist at Freddie Mac, says:

“The decline in mortgage rates does increase prospective homebuyers’ purchasing power and should begin to pique their interest in making a move.”

As a next step, ask yourself this: what number do I want to see rates hit before I’m ready to move?

Maybe it’s 6.25%. Maybe it’s 6.0%. Or maybe it’s once they hit 5.99%. The exact percentage where you feel comfortable kicking off your search again is personal. Once you have that number in mind, you don’t need to follow rates yourself and wait for it to become a reality.

Instead, connect with a local real estate professional. They’ll help you stay up to date on what’s happening and have a conversation about when to make your move. And once rates hit your target, they’ll be the first to let you know.

Bottom Line

If you’ve put your moving plans on hold because of higher mortgage rates, think about the number you want to see rates hit that would make you re-enter the market.

Once you have that number in mind, let’s connect so you have someone on your side to let you know when we get there.

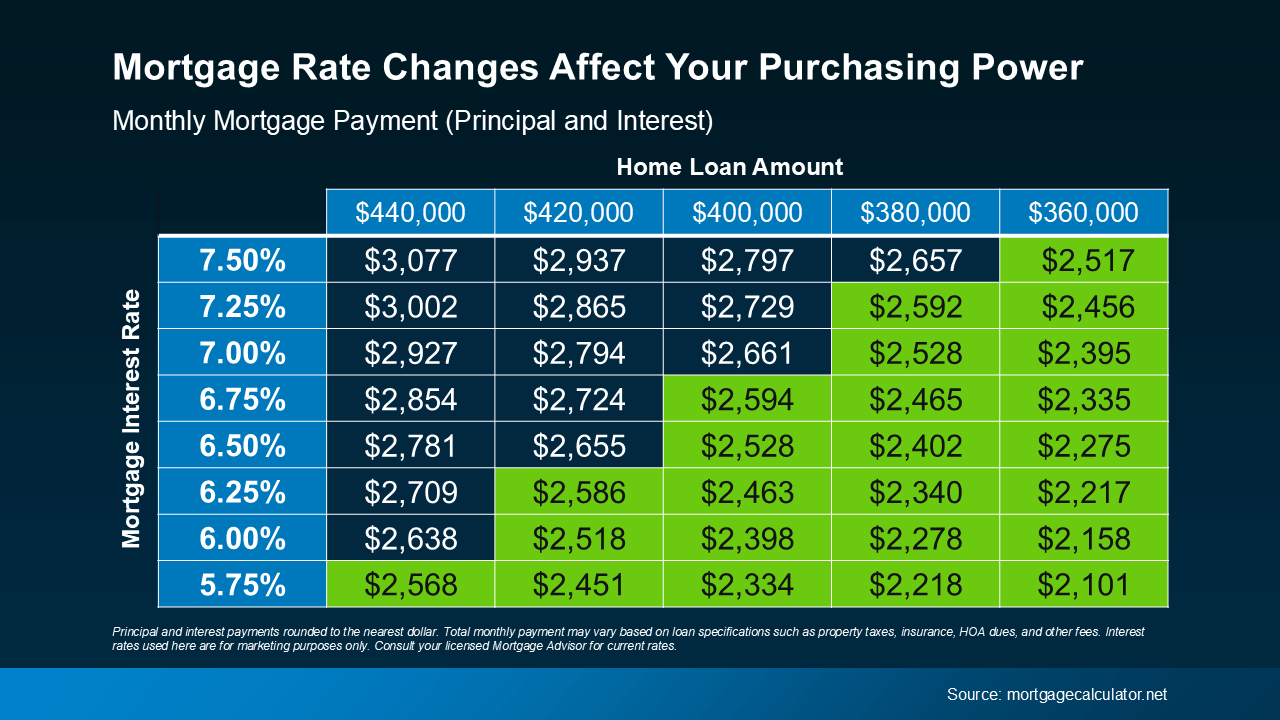

How Mortgage Rate Changes Impact Your Homebuying Power

If you’re thinking about buying or selling a home, you’ve probably got mortgage rates on your mind. That’s because you’ve likely heard that mortgage rates impact how much you can afford in your monthly mortgage payment, and you want to factor that into your planning. Here’s what you need to know.

What’s Happening with Mortgage Rates?

Mortgage rates have been trending down recently. While that’s good news for your homebuying plans, it’s important to know that rates can be unpredictable because they’re affected by many factors.

Things like the economy, job market, inflation, and decisions made by the Federal Reserve all play a part. So, even as rates go down, they can still bounce around a bit based on new economic data. As Odeta Kushi, Deputy Chief Economist at First American, says:

“The ongoing deceleration in inflation, coupled with the Federal Reserve’s recent indication of potential rate cuts [in 2024], suggests an environment supportive of modest declines in mortgage rates. Barring any unforeseen circumstances and resurgence in inflation, lower mortgage rates could be on the horizon, but the journey towards them might be slow and bumpy.”

How Do These Changes Affect You?

When mortgage rates change, it affects how much you pay each month for your home loan. Even a small rate change can make a big difference to your monthly bill.

Take a look at the chart below to see how different mortgage rates impact your house payment each month for various loan amounts. Imagine you can afford a monthly payment of $2,600 for your home loan. The green part in the chart shows payments in that range or lower based on varying mortgage rates (see chart below):

Understanding how mortgage rates impact your payment helps you make better decisions.

How Can You Keep Track of the Latest on Rates?

Real estate agents have the expertise to help you understand what’s happening and what it means for you. They can provide tools and visuals, like the chart above, to show how rate changes impact your buying power.

You don’t need to be a mortgage expert; you just need a professional by your side. Someone who can help you make sense of the market and guide you through your homebuying or selling journey.

Bottom Line

If you have questions about the housing market, let’s connect. That way you’ll understand what’s going on and how to navigate it.

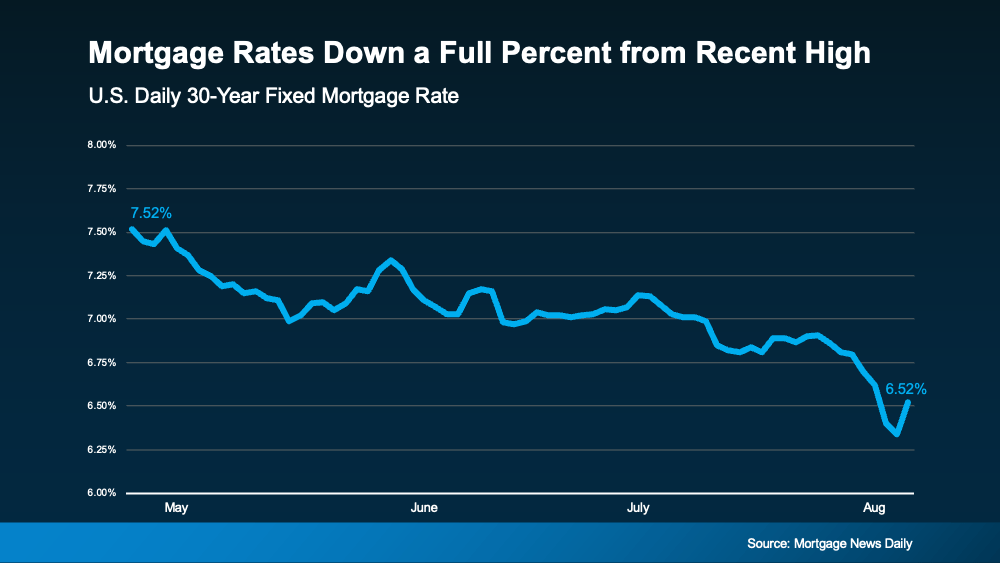

Mortgage Rates Down a Full Percent from Recent High

Mortgage rates have been one of the hottest topics in the housing market lately because of their impact on affordability. And if you’re someone who’s looking to make a move, you’ve probably been waiting eagerly for rates to come down for that very reason. Well, if the past few weeks are any indication, you may be getting your wish.

Mortgage Rates Trend Down in Recent Weeks

There’s big news for mortgage rates. After the latest reports on the economy, inflation, the unemployment rate, and the Federal Reserve’s recent comments, mortgage rates started dropping a bit. And according to Freddie Mac, they’re now at a level we haven’t seen since February. To help show the downward trend, check out the graph below:

Maybe you’re seeing this and wondering if you should ride the wave and see how low they’ll go. If that’s the case, here’s some important perspective. Remember, the record-low rates from the pandemic are a thing of the past. If you’re holding out hope to see a 3% mortgage rate again, you’re waiting for something experts agree won’t happen. As Greg McBride, Chief Financial Analyst at Bankrate, says:

“The hopes for lower interest rates need the reality check that ‘lower’ doesn’t mean we’re going back to 3% mortgage rates. . . the best we may be able to hope for over the next year is 5.5 to 6%.”

And with the decrease in recent weeks, you’ve got a big opportunity in front of you right now. It may be enough for you to want to jump back in.

The Relationship Between Rates and Demand

If you wait for mortgage rates to drop further, you might find yourself dealing with more competition as other buyers re-ignite their home searches too.

In the housing market, there’s generally a relationship between mortgage rates and buyer demand. Typically, the higher rates are, the lower buyer demand is. But when rates start to come down, things change. Buyers who were on the fence over higher rates will resume their searches. Here’s what that means for you. As a recent article from Bankrate says:

“If you’re ready to buy, now might be the time to strike. Home prices have been rising primarily because of a longstanding shortage of homes for sale. That’s unlikely to change, and if mortgage rates do fall below 6%, it’s possible buyers would enter the market en masse, further pushing up prices and resurrecting bidding wars.”

Bottom Line

If you’ve been waiting to make your move, the recent downward trend in mortgage rates may be enough to get you off the sidelines. Rates have hit their lowest point in months, and that gives you the opportunity to jump back in before all the other buyers do too.